Author: twentytwo

As viewings in person of the properties we are marketing are currently not possible, make your first viewing a virtual one!

On our website you will see next to many of our properties the opportunity to view a rolling video comprising all the beautiful professional photographs taken inside and outside the property.

Our agents have also been busy making their own video walk-throughs of our For Sale properties, many of which you can be viewed on our branch facebook pages and are now also starting to appear on our very own YouTube channel

Our agent videos present a more three-dimensional look inside each of the properties as well as a good idea of the location and setting of each property.

Our agent videos present a more three-dimensional look inside each of the properties as well as a good idea of the location and setting of each property.

Please call the relevant branch if any of our properties catch your eye. We can fill you in on all the details you will need.

Author: twentytwo

We feel the time has come for us to put the safety of our colleagues, clients and customers first. We have taken the difficult step of closing our offices to visitors with immediate effect unless by prior appointment. Most of our staff will be working from home for the foreseeable future, but the Company remains very much ‘Open for Business’.

Over the next few days our phones will divert to mobiles and we can still be contacted by e-mail. We will be carrying out Market Appraisals by video and we are producing viewing videos of our properties which can be e-mailed to you or viewed on our social media channels.

We thank you for your understanding and send you and your family our best wishes at this difficult time. Stay safe, stay well and keep social distancing.

Author: twentytwo

Whilst the Corona Virus continues to spread further across the country, we are maintaining a calm and practical approach to this issue but also taking our responsibilities to our staff and our customers very seriously.

If you are elderly, have an underlying health issue or are just concerned about visits to your property we are happy to revisit to make a short video to replace a ‘first viewing’. This would be e-mailed to the potential buyers and, if appropriate, shared on our social media. Those most interested could then be invited to view in person.

We would respectfully ask for our staff to be able to wash hands with soap and water at the beginning and end of the viewing in the absence of hand sanitiser which is very hard to obtain. Our viewers would carry their own personal towel for this purpose. We would ensure that the viewers do not touch surfaces, door handles etc.

As a team, we are adhering to best practice guidelines provided by the Government and Public Health England.

We hope you will feel the steps we are taking so far are understandable:

- We are operating a ‘no shaking hands policy’

- We are encouraging our customers to contact us by phone, email and social media where possible and avoid unnecessary visits to our offices

- If you have recently returned from one of the high-risk countries detailed on the Government website, we would respectfully ask you to contact us by phone or email rather than coming to our offices.

- If you are a client (tenant, potential buyer, seller or landlord) and are self-isolating upon official medical advice, please make us aware before making arrangements for an office or home appointment.

Please contact us if you have any concerns or questions. In the meantime, we thank you for your co-operation and understanding.

Author: twentytwo

Last week Phillip Bishop was interviewed by Tim Thurston for community radio station Swindon 105.5.

Selling or buying a property is a complex process and as a nation, because we are moving home less often, when we do decide to take the plunge few of us are up to speed on all that’s involved.

Phillip provides a helpful reminder of the key things to bear in mind when making what for most of us is our biggest purchase. Great advice hear for anyone who hasn’t moved in a while as well as those buying their first ever property.

Click here to listen now.

If you are looking to upsize, downsize or buy your first ever property take a look at what’s on the market with Perry Bishop and Chambers, one of the region’s leading independent estate agents with branches serving Gloucestershire, Oxfordshire and Wiltshire.

Author: twentytwo

If you are buying a home in England costing more than £125,000, you will have to pay Stamp Duty Land Tax on the purchase of your new home. In the provinces, it’s called something slightly different, so if you are buying a property in Scotland over £145,000 you will pay Land and Buildings Transaction Tax (LBTT) and for any property over £180,000 in Wales you will pay Land Transaction Tax (LTT). Whatever the tax is called, it is an important factor when moving, when you consider that

Last year the average UK house buyer paid £10,150 in Stamp Duty Tax alone

Now as soon as the date for Rishi Sunak’s budget was set for 11th March 2020, conjecture in the Press began about what stamp duty changes he may disclose on budget day. The Chancellor only sets the budget for England and Northern Ireland, yet this is just as relevant for Wales and Scotland. Even though Derek Mackay, the Scottish Finance Secretary said on 6th February he has no plans to change Scotland’s version of Stamp Duty (LBTT), more often than not, Stamp Duty rule changes in England are often adopted in Wales and Scotland at a future date.

Some are asking if Sunak will impose what was promised in the Conservative manifesto with the 3% additional Stamp Duty surcharge on non-UK resident buyers? I have certainly heard in the Estate Agent community that foreign buyers are trying to rush through their sales in central prime London (Park Lane/Mayfair etc etc) before 11th March to ensure they don’t get hit with a new tax. Or will he go even further, and will we see a reappearance of Boris Johnson’s hitherto specified aim of eliminating Stamp Duty below £500k, consequently theoretically saving homebuyers many thousands of pounds?

However, opinions are divided on what, if anything, will be included in the budget. Most believe that the extra 3% for foreign nationals is an almost certainty, and if it isn’t implemented straight away, it will be in the Autumn Statement. Many believe the Chancellor could also decide to repay the favour to those in the North who turned the Election map ‘blue’ on the evening of 12th December with actions to enhance the housing market north of the M62 with stamp duty changes. The best way he could do that is to raise the threshold from the current £125k.

When Boris ran for Tory leadership back in May 2019, he said that he wanted to expand the threshold at which you begin paying stamp duty from £125k to £500k, which when you consider 7 out of 8 residential sales in 2019 were for homes below £500k, that would have a considerable effect. If the Stamp Duty threshold had been raised to £500k in 2019, then 700,400 homebuyers in England would not have paid any Stamp Duty Tax.

84.3% of Faringdon properties sold last year were below £500k

Of the 248 properties sold in the last 12 months within a 3-mile radius of Faringdon, only 39 of those properties sold were over £500,000 (interesting when compared with Greater London where 44.9% of properties were below the £500k level).

Yet the cost to the HM Treasury would be significant. If all properties below £500k were exempt, the government would lose £2.22bn in tax receipts according to Savills. Of course, this could be made up with extra tax on empty properties or increasing the second homes Stamp Duty levy from the current 3% to say 5%, which would raise an additional £1.12bn on top of the current £1.68bn it raises for the Treasury, yet it would have a negative effect on buy-to-let landlords buying additional homes.

What almost unquestionably won’t happen is the earlier idea of switching the Stamp Duty liability from homebuyer to home seller

This would stall the property market, would probably cause political fallout among 688,300 homebuyers who paid Stamp Duty last year alone, make homes ‘appear’ more expensive as house sellers would inflate the asking price to try and recoup some of the tax, yet ultimately could be seen as ‘re-arranging the deckchairs on the Titanic’.

The 3% additional levy for foreign buyers is almost certain (of which we don’t get many in Faringdon – as they tend to buy in prime London areas which is of course the City of Westminster and the Royal Borough of Kensington & Chelsea, and parts of the boroughs of Hammersmith and Fulham, and Camden), yet I have a feeling that ultimately the Government doesn’t want to rock the boat on the wave that is being rode by the property market on the ‘Boris Bounce’ since December. I also doubt any changes will be made to first time buyer Stamp Duty relief, as 22% of all property transactions in 2019 were to first-time buyers, and whilst it cost the Treasury (or saved the first-timer buyers) a total of £539m in Stamp Duty relief (an average of £2,411 each), the Government are keen for first time buyers to get onto the housing ladder.

Ultimately, we can only wait until Mr Sunak opens his red leather box on tomorrow to find out what will happen. I will of course report back after the budget on what (if any) changes to the tax regime will affect the Faringdon property market going forward.

Author: twentytwo

MD Phillip Bishop looks ahead to the March Budget. The year has started well in the property market, but what could the Chancellor do to really get things moving?

On the 11th March, Budget Day, all eyes will be on our new Chancellor of the Exchequer, the Rt Hon Rishi Sunak MP.

One group of English taxpayers will be especially interested in what, if any, changes there are to Stamp Duty. This tax is payable by those buying property over £125,000 – although first-time buyers aren’t liable for stamp duty on homes up to £300,000. The taxation for Scottish and Welsh homebuyers is slightly different.

With the average house price in the UK now £234,742, this stamp duty affects a great many homebuyers. So much so, that over the 2018/19 tax period, the government collected almost £12 billion in stamp duty revenue. A cynic might think, small wonder the government is actively persuading the population to buy homes.

But the problem with high stamp duty is that it does the opposite. It deters people from moving – prevents people in larger homes, they don’t need, from downsizing and selling to people who do need them. It stalls the market and prevents a natural flow of discretionary buying and selling.

A previous Tory plan was to overhaul stamp duty by raising the threshold from £125,000 to £500,000 and lower the top rate – which applies above £1.5m – from 12% to 7%. But this was dropped from the last election manifesto. Could the Chancellor resuscitate this policy? It would greatly help the housing market if he did.

Although the introduction of a mansion tax is looking unlikely, overseas buyers will worry that the Chancellor will introduce a 3% stamp duty surcharge. This tax would include ex-pats wanting to move back home – after Brexit, more likely than for many years. This levy would be on top of stamp duty already payable, including the 3% surcharge on second homes and buy-to-let properties.

Successive chancellors might not have been precisely helpful to the housing market. Now that this government seems keen to build infrastructure, perhaps they will be inclined to treat housing – and flood defences – with the same importance the population does. Railway lines may be necessary but aren’t good homes and a buoyant property market more so?

Author: twentytwo

In the latest, and most recently published, set of UK mortgage data (for the month of November 2019) 18,470 pound-for-pound re-mortgages were made (i.e. the borrower went from one rate to another with no additional borrowing).

However, since the 1970s, the British have seen their homes as cash cows and cash machines, with many homeowners re-mortgaging at the end of their mortgage’s introductory term (usually after the initial two, three or five years) to avoid being passed on to their mortgage lender’s more expensive standard variable rate.

For some borrowers re-mortgaging allows them an opportunity of raising additional cash whilst for others it enables them to follow interests and activities; such as big holidays, home improvements, new cars, debt consolidation or financially helping family members (e.g. paying off credit cards or helping with house deposits).

Interestingly, in November 2019 alone (the most recent figures) an eye watering £957,856,700 was borrowed on top of existing mortgages by 18,610 UK homeowners re-mortgaging and borrowing, on average, an additional £51,470. Therefore, one has to ask, are we borrowing too much? Looking at these numbers, one might think we are over-extending ourselves, yet as regular readers of my blog about the Faringdon property market will know – I like to drill down and look at the historical figures. Back in 2006, just before the crash, British homeowners were actually borrowing in excess of £5bn per month over and above the re-mortgage amount – much more than the £1bn we experienced in November!

Looking at statistics from the Bank of England for the UK as a whole, even with the data mentioned above, British property owners have increased the equity in their homes by just over £270 billion since 2010 compared with a £275 billion withdrawal during the 2000s. This reveals that the last decade (the 2010’s) is the first since records began in which Brits have increased their equity. This is partly due to the fact that the number of housing transactions crumpled during the Credit Crunch, and many homeowners chose to reduce their mortgages, rather than continually increasing them – even if their property started going up in value after 2013.

So, what has happened in Faringdon regarding mortgages and does it match the national picture? Well interestingly…

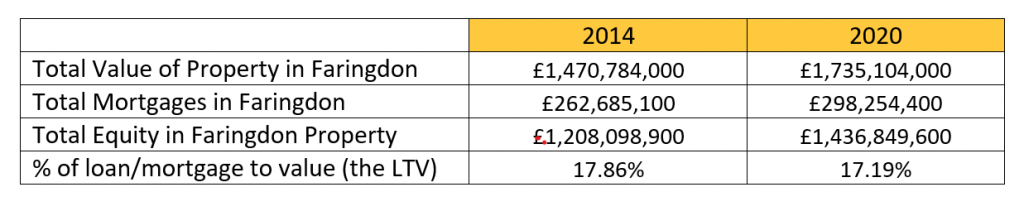

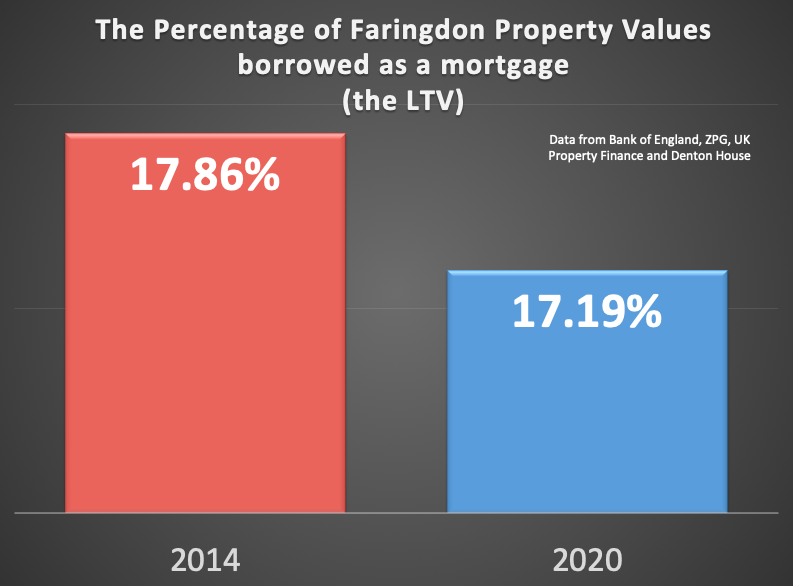

Faringdon homeowners have injected over £200m into their Faringdon properties over the last six years; overturning a trend stretching back to the 1970s.

Considering the exact figures, it can be seen whilst the total value of mortgages has increased slightly since 2014, as a percentage this has gone down slightly, meaning Faringdon homeowners and Faringdon landlords have increased their equity since 2014 by £228,750,700 (one might call it a windfall?).

It can quite clearly be seen that the financial insecurity sparked by the Credit Crunch crisis has created a generation of Faringdon homeowners/landlords who are savers and improvers rather than movers and excessive borrowers, using excess cash to invest in their property and pay down debt or to excessively borrow on their equity growth, as can be seen on the graphs and table.

As the percentage of mortgages (the loan to value) has decreased since 2014 from 17.86% to 17.19% in Faringdon, this is good news for every Faringdon homeowner and Faringdon landlord because, irrespective of whether the ‘Boris Bounce’ is short or long lived, it shows the Faringdon property market is in a better state than ever before to ride out any storm that it might encounter because less people will be in negative equity or have prohibitively high mortgages.

Author: twentytwo

Since the recent General Election gave us a majority Government and the uncertainty of Brexit has at least jumped an important hurdle, there has been a palpable air of positivity running throughout the property industry. Many refer to this as the Boris bounce. David Packwood, Senior Land Manager at Perry Bishop and Chambers, welcomes the return of a more confident market.

Last year has been labelled by many in the industry as a year of resilience as numerous home and land owners sat on the fence, sales plateaued and prices were very sensitive. However, it appears that the mood has changed and confidence has returned amongst buyers and vendors who see 2020 as the year to get on with their lives.

The number of First Time Buyers has reached its highest level since 2007, taking advantage of relatively low mortgage rates, Stamp Duty Relief and new homes schemes such as Help to Buy and last week Rightmove reported its busiest ever month with record numbers of home movers looking for property.

Last year’s ‘wait and see’ behaviour was also very much in evidence amongst landowners and developers . However, since the start of the year the Perry Bishop and Chambers’ specialist land department have experienced a surge of interest from landowners contacting them looking to sell – a very welcome and positive sign.

However, demand continues to outstrip supply and so David and his team urge more landowners to contact them to capitalise on this wave of buyer momentum.

Perry Bishop and Chambers’ dedicated and much respected Land and Development service benefits land owners and developers alike, offering a comprehensive marketing service for single building plots, development sites and buildings for conversion. Bringing to market an array of opportunities from across Gloucestershire, Oxfordshire, Wiltshire and beyond, the team is headed up by company director Peter Chambers and Senior Land Manager David Packwood.

David Packwood will be speaking at the Buy-to-Let and Property Development 2020 seminar at Cowley Manor, Cheltenham on 4th March.

Call the team on 01285 646770 for your free initial appraisal and planning advice.

Author: twentytwo

The door is now open to easier development opportunities.

Recent changes to Permitted Development rights mean that converting agricultural buildings into residential properties is now far simpler than ever before. Now rural landowners no longer need to apply for planning permission to convert barns to residential, school or nursery (childcare) use.

In summary, the order creates a new class of permitted development ‘Class MB’, which allows change of use from agriculture to residential use.

Prior to the announced changes a barn could be converted to provide up to 3 new homes within a maximum of 450 square metres, the new changes allow:

up to 3 larger homes within a maximum of 465 square metres

or

up to 5 smaller homes each no larger than 100 square metres

or

a mix of both, within a total of no more than 5 homes, of which no more than 3 may be larger home.

For further clarification on this new ruling please contact the region’s leading land and development service on 01285 646770 to discuss your options and learn how you can realise the true value of your agricultural buildings.

Example of redundant barn sold by our Land and Development team

Barn now converted to sell by our Cheltenham branch

Author: twentytwo

Perry Bishop and Chambers are delighted to extend their exceptional property marketing service to people on the move across North Wiltshire. Experienced estate agent Caroline Ferris has been appointed Associate Partner to head up valuations and sales across this extremely convenient and sought after location comprising Chippenham, Malmesbury and Corsham and all the delightful villages in between.

“I am so pleased to be able to be able to offer a very personal service to people looking to move in and around the area where I live,” says Caroline who lives in the village of East Tytherton, just outside Chippenham. “It’s brilliant news that anyone living in the towns and villages in this beautiful part of the world can now take advantage of Perry Bishop and Chambers’ award-winning estate agency service.”

If a move is on the cards for 2020 – maybe an extra bedroom is now a necessity for your growing family or conversely you may no longer need so much space – that’s where Caroline and the team at Perry Bishop can help. Our bespoke 11-Step Plan – based on proven results of selling hundreds of properties – offers the perfect strategy for attracting the right buyer for your property and achieving the best price, typically an additional 2% more than the average sales price.

Meet Caroline:

Caroline has lived in North Wiltshire for 35 years, married in Sutton Benger and has raised three children. She has a great understanding of the local area, with 14 years’ experience, as an estate agent in both Gloucestershire and Wiltshire. She is well equipped to offer professional, expert and friendly advice in all aspects of property sales and her enthusiasm and dedication ensure exceptional service throughout the sales process.

In her spare time, as a great lover of the outdoors she enjoys walking her dogs and anything to do with horses! Her grown up family live nearby and spending quality time with her two grandsons is very important.