Author: twentytwo

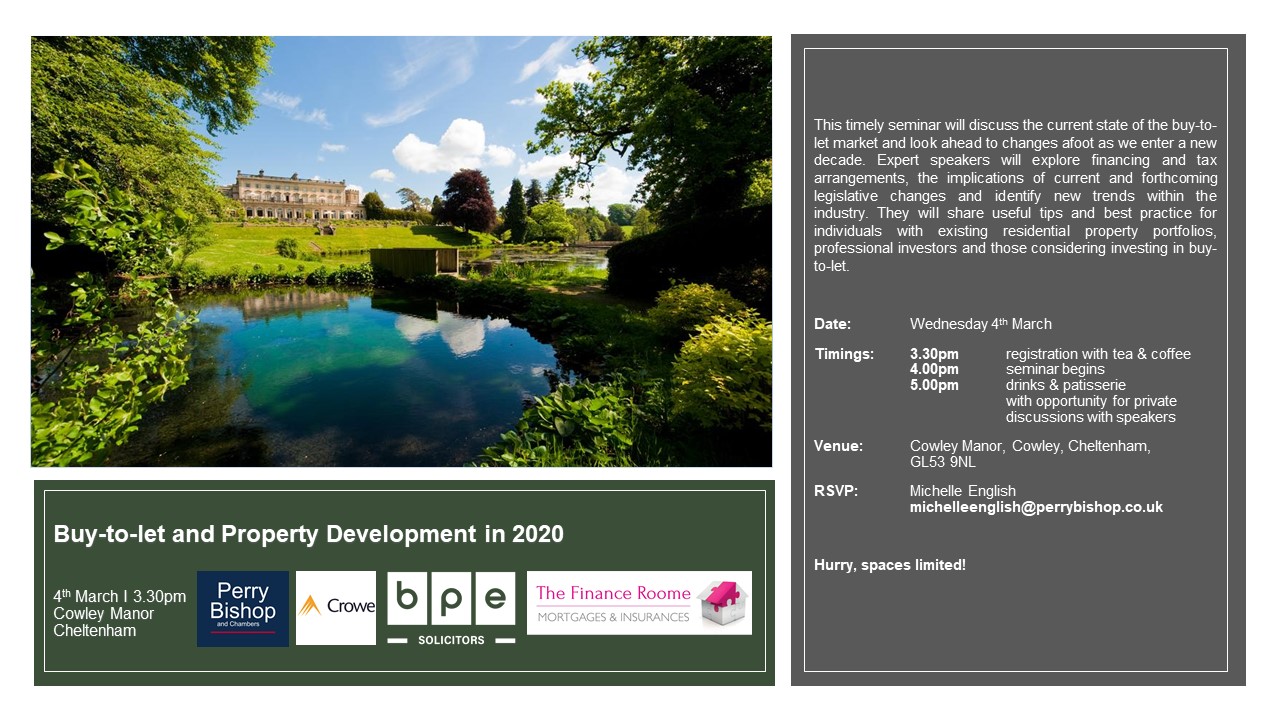

Join us at Cowley Manor, Cheltenham, on Wednesday 4th March for our timely seminar – Buy to let and Property Development in 2020. Expert speakers from Crowe Clark Whitehill, BPE solicitors and The Finance Roome will be joining members of Perry Bishop and Chambers lettings and land teams to consider the current state of the industry and review changes afoot.

This free of charge event is essential for all landlords and property investors – providing the very latest info on financing and tax arrangements, lettings legals and new trends within the sector.

We have limited spaces, so please RSVP as soon as possible to reserve your spot.

Date: 4th March 2020

Time: 3.30pm – registration with teas and coffees

4.00pm – seminar starts

5.00pm – drinks and patisserie

Venue: Cowley Manor, GL53 9NL

RSVP: michelleenglish@perrybishop.co.uk

We look forward to seeing you there!

Author: twentytwo

Ah the 2010’s, the tens, the teens – I am not sure what we are supposed to call the decade that has just gone. No matter what it was called, the last decade was a tough one, so does it really matter that we never really got around to giving it a name? Some might say, whatever one calls it, coming to an end is the most fundamental job any teen (and I refer to all humans) could possibly do!

The last two decades have certainly been tumultuous. At least for this decade we have just started we can say, in a few decades time, things like “That style is so ’20s” and fellow humans will essentially know what you are talking about. If you come of age in this decade, you will be a ’20s child and we will discuss ’20s politics and ’20s style and all the things that hadn’t been created on the 31st December 2019; the time that two nameless decades ended and how finally there was something everyone in the UK could agree on: the name of the decade. Hey – it’s a start!

So, what has happened to the local Faringdon property market in the last nameless decade?

The average Faringdon property has risen in

value from £253,800 to £387,300 in the last 10 years

…meaning each Faringdon homeowner has seen a profit of £256.73 per week for those last ten years. Rolling the clock back to the start of the last decade January 2010, and the economy (and housing market) were recovering from the Credit Crunch and the worldwide financial crisis. A decade on and things feel a little different. If you bought a Faringdon home over the past 10 years, things have certainly changed.

Faringdon property values rose 52.6% on

average over the last decade

yet taking inflation into account, they only rose in real terms by 19.6 per cent.

Compare that to a 42.5% rise in the ‘80s, a 13.2% drop in the ‘90s and rise of 62.8% in the 2000s in real terms. So, in real terms after inflation, there has been less of a house price growth in Faringdon in the past decade than the previous one.

On average, 1.12 million homes were sold each year last decade, although that was 26.4% less than the decade before (the noughties) when an average of 1.52 million properties were sold annually.

So, what are the underlying issues in the Faringdon (and wider UK) property market when, in real terms, property is 19.6% more expensive than a decade ago? Whilst the newspapers tell us first time buyers can’t get on the housing ladder and the housing market is in gridlock – what is the problem? Well I am a firm believer in the adage ‘bad news sells newspapers’ because the truth is something completely different as 32.7% of homes last year were bought by first time buyers compared with only 22.8% in 2009.

Yet, there are still issues; mainly a persistent lack of not building enough new homes which curtails the supply and choice of property; but stagnated wages, stiffer mortgage rules and homeowners not moving as much as previous generations are all contributing to the problem. In the UK, the number of homeowners who moved in 2019 was around 14% higher than in 2009, yet this was still just under 50% lower than the average for the noughties. It’s all up and down like a rollercoaster!

My thoughts for the future are based primarily on what will happen to interest rates. Throughout the last decade, the Bank of England base rate was 0.5% at the start and was cut to 0.25% in the Summer of 2016. Even with the increase to its current level of 0.75% in the Summer of 2019, it has made borrowing money on a mortgage very cheap indeed. Nonetheless, bank/mortgage rates will rise again and I am concerned about the effect upon the housing market. Now it won’t be as bad as previous times when mortgage rates went up in the 1970’s and 1980’s (with mass repossession) because the tougher mortgage rules introduced in April 2014 will have ensured borrowers were stress tested on their affordability if interest rates shot up. Most borrowers have been stress tested on their affordability to mortgage rates of up to 6% – 6.5%, which would obviously squeeze household disposable incomes yet stop people losing their homes due to repossession. Whilst I am not giving advice, just personal opinion, if you are one of the 29.3% of homeowners who isn’t on a fixed rate – maybe you should seriously consider doing so?

The 2020’s will be an interesting decade – and if you want to be kept up to date with what is happening in the Faringdon (and wider UK) housing market – follow me and this blog to read similar articles to this one.

Author: twentytwo

The Halifax announced in early January that there was a Boris Bounce in the national property market as they stated national property values soared 1.7% in December 2019 – the biggest rise since the 1.9% month on month rise in February 2007 (a few months before the Global Financial Crisis aka the Credit Crunch).

Get the flags out – all hail Boris as the Conservatives gain their landslide general election triumph – the Boris Bounce is here … or is it?

The Halifax (as well as the Land Registry and other house price indexes) use data of property that has sold and completed (completion being when monies and keys of homes sold are transferred). The Halifax data was based on properties that completed in December 2019, and as anyone who has sold or bought a Faringdon property in the last 10 years knows, the time it takes from agreeing a buying price to handing over the money is many weeks. In fact, the average length of time between sale agreed and completion in the country is running at 19 weeks, meaning the figures mentioned by the Halifax are for sales agreed in July / August 2019. This growth relates to what was happening to the property market in Summer 2019.

One of the most important things for the property market is confidence. Interestingly, Rightmove reported a 28% surge in buyer enquiries between the 13th December and 18th December. After a couple of years of Parliamentary hold-up, the confidence following this general election is unquestionably a much needed boost for the economy (and ultimately confidence), so much so, shares in the new homes builders Barratt jumped 14% and Persimmon 12% the day after the election, showing a property sector anticipation that the property market is about to move forward as suppressed demand for people moving home is liberated.

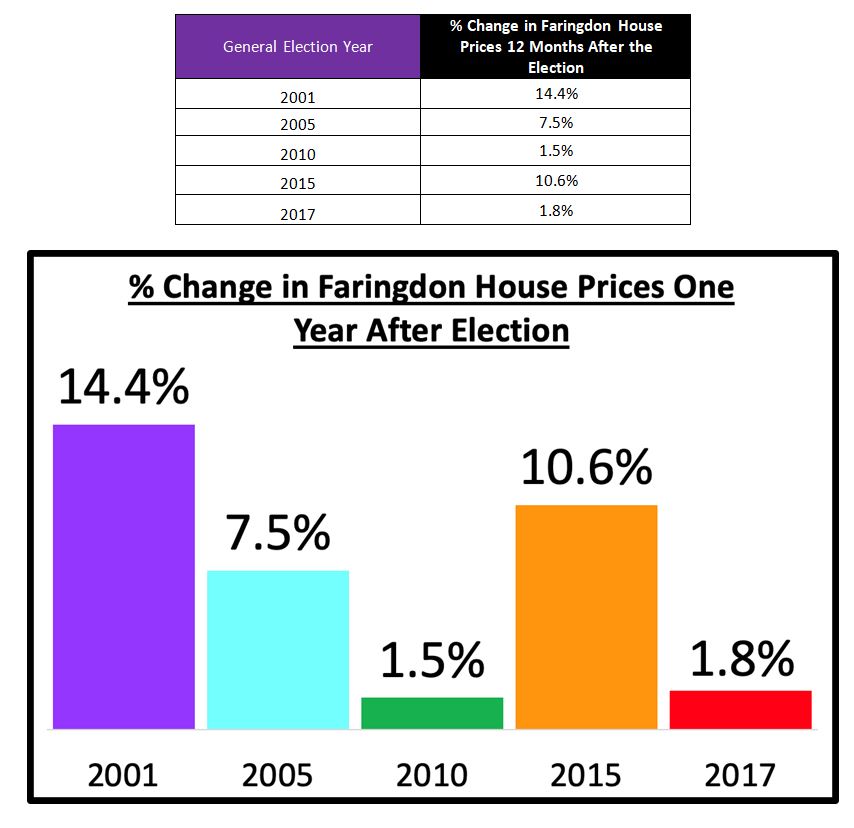

Looking at the previous elections, I decided to look at what happened to property values in Faringdon in the 12 months after each election, with some interesting results.

So, with past experience, a general election generally has a good effect rather than a worse effect on the Faringdon property market.

Looking at the rest of 2020, my intuition tells me in the better areas of Faringdon, it will likely be a seller’s market, as they will have more influence to ask for higher asking prices from Faringdon property buyers that have placed plans to move on hold for far too long – and this could push up Faringdon property values more promptly in the short term.

Yet, as more Faringdon properties come on to the market in the usual spring rush, we could see Faringdon home buyers having more choice and thus, as supply increases yet demand remains the same, buyers will get more power to negotiate a better deal. Irrespective of that, there is still the all-encompassing issue that I have spoken about many times in my blog of not enough homes being built to keep up with the number required, meaning negotiating power and prices being inflated.

The bottom line is, the Faringdon housing market will get a slight boost from the general election. The threat of a Jeremy Corbyn government obstructed some Faringdon landlords to build their buy to let portfolio in the later parts of 2019, so as long as sellers remain realistic with their pricing and present their properties in the best light, 2020 in the Faringdon property market should be a year of ‘steady as she goes’.

P.S .One final thought – remember what I said about the Halifax price Index being 5/6 months behind the times – don’t be alarmed when they announce in the March/April/May a reduction in property values – like I said before – this will be the prices achieved in the later parts of 2019 i.e. not what is happening right now.

Author: twentytwo

We have started the year enjoying the effects of a ‘Boris Bounce’. New buyers are flocking to the market, registering their interest and actively viewing available properties matching their requirements. New stock is coming to the market every day and it will not be long before the days start to lengthen and temperatures warm. So what steps can you take to make sure your home stands out above the competition and you attract the best buyers.

1. KERB APPEAL

Sixty seconds is all it can take for a potential buyer to decide they want to view your home or not. You want as many buyers as possible to cross your threshold, thus maximising your chance of securing the best buyer and the best price. Your front garden should be tidy and weed free. Trim back any overgrown vegetation and invest in fresh spring planters to place by your front door. Move cars and bins off the drive and leave plenty of space for your viewers to park. Finally make sure your front door shines – give it a good clean and touch up paintwork if necessary.

2. DECLUTTER

Pack up surplus furniture and personal items – hire a storage unit or put them in the loft. Clear shoes and coats from the porch, hall or cloakroom leaving these spaces feeling bigger. Bedrooms should be clear of yesterday’s clothes and shoes, books and papers, make up and jewellery. In bathrooms remove surplus make up, cosmetics, shower and bath products and change towels and bath mats for fresh, clean or brand new ones. Taps and surfaces should be cleaned and sparkling and the room well ventilated. Kitchen surfaces need to be as clear as possible creating maximum worktop space. Remove any pet bowls, sinks should sparkle and check for last night’s cooking smells! Tidy shelves.

3. SPRING CLEAN!

Your house needs to be scrupulously clean inside and out. Get out the duster and check all nooks and crannies. Don’t forget ceilings, light shades and dust all surfaces. Clean windows and mop floors. Keep your home tidy for those last minute viewings.

4. DIY

Buyers like a well kept and maintained home – they want to be able to just move in, unpack, and start enjoying their new home. Take a long hard look – have you finished all those DIY jobs you know need doing? Tackle them now and make sure all your light bulbs work, dripping taps are fixed and squeaky doors are oiled. Does the doorbell work and do all doors and windows close properly? Touch up paintwork and show your buyers your home has been well cared for.

5. Freshen Up

Visitors to your home should be greeted by the smell of fresh flowers or fresh air, not pets, smokers or last night’s cooking odours. Rehome your pets on viewing days, send smokers outside and keep all doors and windows open when cooking. Avoid fish and curry when you are trying to sell your home! Burning a scented candle helps to neutralise these odours or use a discreet air freshener.

6. Give your viewers space and privacy

On a dull day put turn on the lights and leave the heating on. If your viewers view your home when it is cold, they will always imagine it being cold.

Your buyers will be shown around your home by the agent and they need to be able to wander and get a feel for the place, to make comments out of your hearing and to discuss what works and what doesn’t work for them. The agent is trained to help overcome objections and to encourage an offer or second viewing. Go out if possible, if not, leave them alone. Your buyers will feel more relaxed and are more likely to make you an offer.

Finally, ask a friend or your agent to be brutally honest about what might need attention. Follow the advice and make sure your home is correctly priced. Before long, you will be on the move!

Author: twentytwo

Phillip Bishop, MD at Perry Bishop and Chambers, responds to the dramatic start to the new property year and looks at the green shoots of improvement.

Like early snowdrops, property buyers have begun poking their heads above ground after a long period of slumber. In fact, in some parts of the UK, there are significant and spectacular drifts of these ‘snowdrops’ appearing. Is this because of the time of year? Partly: but more likely because we are emerging from an extended and dark period of lifelessness in the property market.

Call it the Boris or Brexit Bounce if you like, but whatever term you give it there is a definite surge in the market with markedly more interest and activity. All over the country numbers of registrations, viewings, offers and sales are up on the previous two or three years – and it’s only February.

Confidence should be the name given to the first physical brick laid in any house construction or metaphorical brick laid in the re-building of the property market. It is confidence that is driving this newfound interest, and it comes at a perfect time of the year.

There was concern that a December election would be harmful in multiple ways. Well, in the case of the property market, it was perfect. With the will-we/won’t-we Brexit issue settled a large cloud of uncertainty was lifted and those who were sitting on their hands have, post-New Year, suddenly jumped into action.

Behind this energy is several years of pent up demand. Those who could wait to make a move or who were nervous did wait. But now the waiting is over. In all sectors of the market and across all regions demand is higher than it has been for years.

This is all exciting stuff, but we should not get too carried away. In property confidence can soon give way to over-confidence, with sellers often eager to set higher asking prices. We don’t want to see all those snowdrops droop under an ill-considered layer of expectation.

So prudence and guidance are critical factors in sustaining this excellent start to 2020. As always, before embarking on selling and or buying a property, we advise seeking the wisdom and counsel of a mature and experienced local independent estate agent before you join the fray. We’d love to help and advise you – do please call your local Perry Bishop and Chambers office.

Author: twentytwo

So you’re probably thinking about selling your property soon or maybe you have a property currently for sale?

Obviously, you want to sell for the best price and to the best buyer. Follow our bespoke 11 Step Plan – comprising all that we have learned from selling hundreds of properties – and you will almost certainly achieve the best price for your property in the shortest amount of time.

It really does work! Here at Perry Bishop and Chambers we implement this exact plan on every property we sell and on average, we achieve 2% more than the average sale price.

Want to find out more? Click HERE to read our structured plan and strategy and discover the formula for selling for a premium price.

Author: twentytwo

So you’re probably thinking about selling your property soon or maybe you have a property currently for sale?

Obviously, you want to sell for the best price and to the best buyer. Follow our bespoke 11 Step Plan – comprising all that we have learned from selling hundreds of properties – and you will almost certainly achieve the best price for your property in the shortest amount of time.

It really does work! Here at Perry Bishop and Chambers we implement this exact plan on every property we sell and on average, we achieve 2% more than the average sale price.

Want to find out more? Click HERE to read our structured plan and strategy and discover the formula for selling for a premium price.

Author: twentytwo

Faringdon House Prices Have Risen by 133% as a Proportion of Household Income since 1980.

Have the Baby Boomers (people between the ages of 55yo to 75yo) messed things up for the Millennials in terms of getting on the Faringdon property ladder? They bought their own council houses in the 80’s and 90’s, meaning there are no affordable homes for today’s youngsters, thus driving up the demand for rental homes and the price of homes (making them unaffordable). So, I decided to look at the figures, which do not make for good reading.

In 1980, the average Faringdon household income was just under £6,000 per annum and the average Faringdon house price was £30,589; whilst today, the average Faringdon household income is £33,200 per annum, yet the average household value is £393,000, meaning…

the average value of a Faringdon home was 5.1 times more than the average household income in 1980 compared to today, where it is 11.8 times a Faringdon household income

… it’s no wonder then that Millennials are pointing the finger at Baby Boomers!

And the problems don’t just stop there. Not only do the newspapers state there is a housing crisis of affordability, but also a crisis of the availability of homes for people to live in. The political parties using housing as a ‘vote getter’ mentioned stats such as in 1981 there were 5.1 million council houses and today that stands at 1.6 million. This is important because, as a substantial number of people will never be able to afford to buy, social housing plays a significant role in homing them.

It all looks rather damning and the phrase ‘OK Boomer’ looks quite apt.

(The phrase ‘OK Boomer’ become fashionable as it started as a way of showing Baby Boomers that things were “easier in the past”, yet now it has become just a way for younger people to discredit the views of older people).

Well, checking the stats, the political parties seemed to forget the number of housing associations homes (which are also social housing) has risen from 0.4m to 2.6m homes in that time, therefore, whilst there is a drop in social housing, it’s a net figure of 2.3m fewer social-rented houses, instead of the 3.5m in the paragraph above.

Baby Boomers simply did the best they could with the circumstances given – it’s not like that these older generations have been conspiring in the food aisles of Waitrose or M&S on how to mess things up for the next generation. There are fundamental underlying problems in British society that means things are difficult for our younger people – it’s everyone’s responsibility to solve those underlying problems – we can’t just blame the Baby Boomers. Millennials aren’t morally superior to Baby Boomers just because they didn’t grow up in the same era of economic growth and house price inflation.

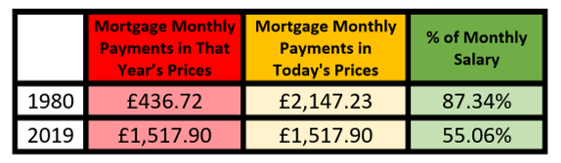

What some people seem to forget is whilst Faringdon property values were lower, so were salaries. The true cost of affordability is the mortgage payments. Assuming someone bought an average property in 1980 and again in 2019, using a 95% mortgage at the prevailing mortgage rate of 17.8% in 1980 and the current 1.65%, today in Faringdon the mortgage accounts for 55.06% of the household income (assuming a single income) compared to 87.34% in 1980. This has to be one of the main reasons why many families became two wage households in the late 70’s/early 80’s as housing affordability was diminished with these eye watering high interest rates.

Things were much tougher for homeowners in 1980….

The issue here is something much deeper. Baby Boomers say it is the Millennials’ own fault they can’t afford to buy their own home because they spend all their money on three holidays, avocado on toast, going out down the pub 3 times a week and buying the latest iPhone or suchlike whilst Millennials accuse the Baby Boomer generation for ruining the housing market ‘per se’ by being selfish. Both are right and both are wrong.

In my own involvement with friends and family, many Faringdon Baby Boomers are trying their best to help out their now grown up children with a deposit. They are fully aware of current Faringdon house prices compared to when they bought their own homes.

I am not a fan of attaching labels, be it Millennials, Baby Boomer or Gen-X. It’s really a point of attitude and behaviour and circumstance rather than the date of your birth. Every generation has had its fair share of feast and famine and whilst I appreciate the irony of the title of this article, let’s stop labelling people and making assumptions, everyone needs to understand each generation’s issues and be more supportive of each other.

Author: twentytwo

Faringdon House Prices Have Risen by 133% as a Proportion of Household Income Since 1980.

Have the Baby Boomers (people between the ages of 55yo to 75yo) messed things up for the Millennials in terms of getting on the Faringdon property ladder? They bought their own council houses in the 80’s and 90’s, meaning there are no affordable homes for today’s youngsters, thus driving up the demand for rental homes and the price of homes (making them unaffordable). So, I decided to look at the figures, which do not make for good reading.

In 1980, the average Faringdon household income was just under £6,000 per annum and the average Faringdon house price was £30,589; whilst today, the average Faringdon household income is £33,200 per annum, yet the average household value is £393,000, meaning…

the average value of a Faringdon home was 5.1 times more than the average household income in 1980 compared to today, where it is 11.8 times a Faringdon household income

… it’s no wonder then that Millennials are pointing the finger at Baby Boomers!

And the problems don’t just stop there. Not only do the newspapers state there is a housing crisis of affordability, but also a crisis of the availability of homes for people to live in. The political parties using housing as a ‘vote getter’ mentioned stats such as in 1981 there were 5.1 million council houses and today that stands at 1.6 million. This is important because, as a substantial number of people will never be able to afford to buy, social housing plays a significant role in homing them.

It all looks rather damning and the phrase ‘OK Boomer’ looks quite apt.

(The phrase ‘OK Boomer’ become fashionable as it started as a way of showing Baby Boomers that things were “easier in the past”, yet now it has become just a way for younger people to discredit the views of older people).

Well, checking the stats, the political parties seemed to forget the number of housing associations homes (which are also social housing) has risen from 0.4m to 2.6m homes in that time, therefore, whilst there is a drop in social housing, it’s a net figure of 2.3m fewer social-rented houses, instead of the 3.5m in the paragraph above.

Baby Boomers simply did the best they could with the circumstances given – it’s not like that these older generations have been conspiring in the food aisles of Waitrose or M&S on how to mess things up for the next generation. There are fundamental underlying problems in British society that means things are difficult for our younger people – it’s everyone’s responsibility to solve those underlying problems – we can’t just blame the Baby Boomers. Millennials aren’t morally superior to Baby Boomers just because they didn’t grow up in the same era of economic growth and house price inflation.

What some people seem to forget is whilst Faringdon property values were lower, so were salaries. The true cost of affordability is the mortgage payments. Assuming someone bought an average property in 1980 and again in 2019, using a 95% mortgage at the prevailing mortgage rate of 17.8% in 1980 and the current 1.65%, today in Faringdon the mortgage accounts for 55.06% of the household income (assuming a single income) compared to 87.34% in 1980. This has to be one of the main reasons why many families became two wage households in the late 70’s/early 80’s as housing affordability was diminished with these eye watering high interest rates.

Things were much tougher for homeowners in 1980….

The issue here is something much deeper. Baby Boomers say it is the Millennials’ own fault they can’t afford to buy their own home because they spend all their money on three holidays, avocado on toast, going out down the pub 3 times a week and buying the latest iPhone or suchlike whilst Millennials accuse the Baby Boomer generation for ruining the housing market ‘per se’ by being selfish. Both are right and both are wrong.

In my own involvement with friends and family, many Faringdon Baby Boomers are trying their best to help out their now grown up children with a deposit. They are fully aware of current Faringdon house prices compared to when they bought their own homes.

I am not a fan of attaching labels, be it Millennials, Baby Boomer or Gen-X. It’s really a point of attitude and behaviour and circumstance rather than the date of your birth. Every generation has had its fair share of feast and famine and whilst I appreciate the irony of the title of this article, let’s stop labelling people and making assumptions, everyone needs to understand each generation’s issues and be more supportive of each other.

Author: twentytwo

Perry Bishop and Chambers’ Cheltenham team have this year chosen local charity – Building Circles – as their Charity Partner for 2020. The estate agents are delighted to lend their support to this brilliant local organisation which gives people with learning disabilities the chance to lead more fulfilling lives through friendship and community participation.

Katie Buck, Office Manager at Building Circles, recently met up Branch Manager Jackie Carlton and the rest of the Cheltenham team at one of their morning training sessions. She talked to them about how Building Circles came about and what they do to help adults with special needs in Gloucestershire – building friendship circles so that they no longer feel lonely or isolated.

Building Circles will benefit from a donation from every house sold by Perry Bishop and Chambers Cheltenham*. Their logo will also appear across all the company’s marketing literature throughout the year. Director, Gavin Wallace, is delighted that Perry Bishop can help raise awareness and much needed funds for the invaluable work of this small local charity. “We are so pleased to be supporting Building Circles in 2020, who provide an invaluable service for people with learning disabilities in our community.”

*Sue Ryder Leckhampton Court Hospice will continue to receive donations from sales of properties in Leckhampton and Charlton Kings.